Key Takeawats:

The APR vs. interest rate conversation continues to confuse those that aren’t familiar with it. However, there is no longer any reason to remain confused yourself. Thanks to the following annual percentage rate and interest rate guide, you, too, will be able to distinguish between these two similar indicators.

Interest Rates & APRs

The APR vs. interest rate debate (if you can even call it that) continues to confound those that are less familiar with the real estate industry. Through no fault of their own, people who aren’t well-versed in the intricacies of investing are confused about the differences between them. In fact, the general public is most likely unaware of many of the differences between them. If for nothing else, the two share enough similarities that I can’t blame anyone who can’t tell them apart. However, it is worth noting that an annual percentage rate and an interest rate are two unique indicators. While they may sound similar, they are anything but.

Several inherent differences exist between interest rates and annual percentage rates, which can be hard to discern for amateur investors. That said, both annual percentage rates and interest rates belong in the common vernacular of today’s most basic investors. Those that can’t distinguish between the two are doing themselves a severe disservice.

If you are — more or less — unfamiliar with the differences that exist between annual percentage rates and interest rates or need a refresher, look no further. The following guide will delve deep into the APR vs. interest rate discussion and give you a better idea of each.

[ Thinking about investing in real estate? Register to attend a FREE online real estate class and learn how to get started investing in real estate. ]

What Is Annual Percentage Rate (APR)?

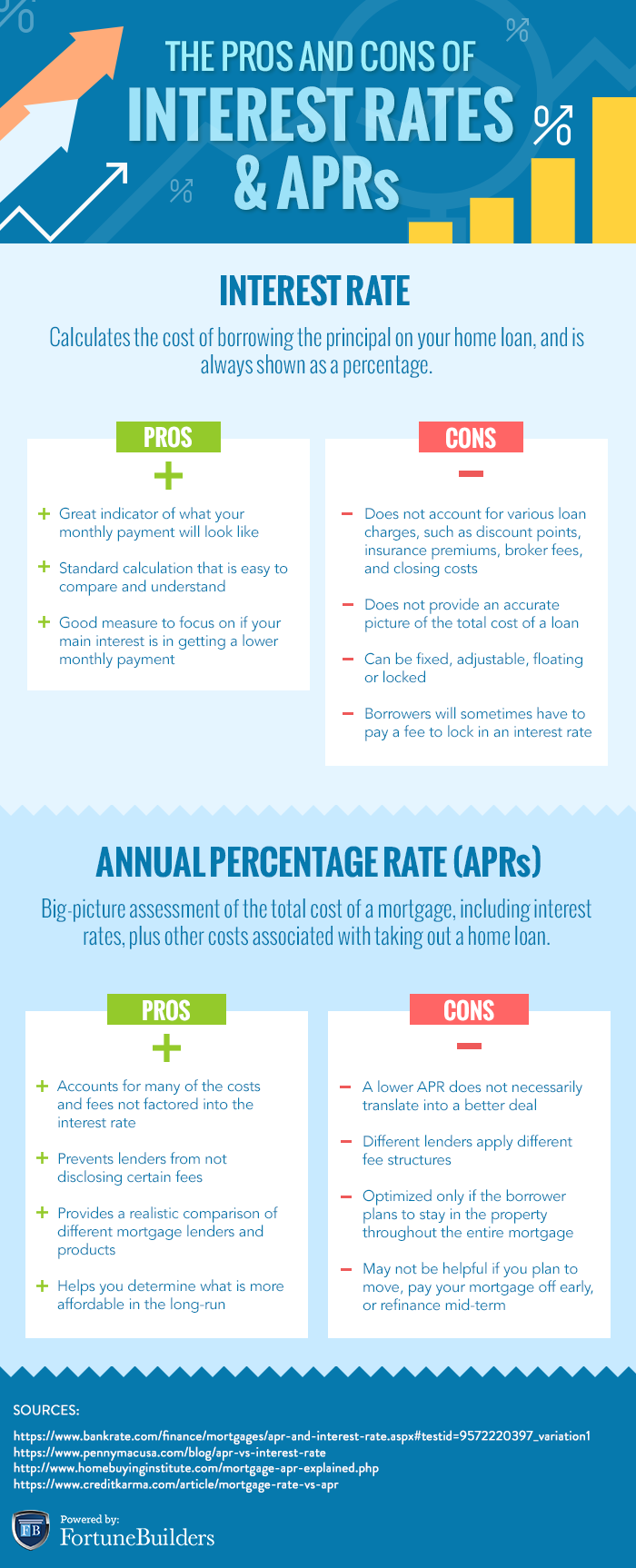

The annual percentage rate, more commonly referred to as the APR, represents the annual rate a person will be charged for borrowing money. As its name suggests, the APR is just that: a percentage rate that identifies the amount it will cost a borrower. Annual percentage rates have become synonymous with most loans, but are most frequently referenced in credit card, auto and — of course — home loans.

It is worth pointing out that the APR includes more than the interest itself; it’s also made up of several additional fees and costs that arise over the course of a loan. However, it is worth noting that the annual percentage rate does not take compounding interest into consideration. Perhaps even more specifically, the APR doesn’t account for the addition of interest to the principal sum. To be clear, the annual percentage rate combines the interest you will pay on a loan with any other costs you will incur from procuring it. As a result, the APR tends to be higher than the interest rate itself.

APR Example

At least for those in the real estate industry, the perfect APR example is not all that different from what many have already experienced. In fact, annual percentage rates have found themselves part of the common vernacular for so many investors that they are essentially a foregone conclusion. That said, here’s an example for those of you looking for a refresher or simply trying to understand what an APR is for the first time:

Say, for example, you want to borrow $100,000 at today’s benchmark interest rate. According to Bankrate, the average 30-year fixed mortgage rate is somewhere in the neighborhood of 4%, and their 15-year counterparts are even lower.

For the sake of this APR example, you are borrowing $100,000 at a 4% interest rate for 30 years. On top of that, you will also find yourself paying additional financing and non-financing fees, which can take the form of closing costs or even transaction fees. Take those additional charges, and add them to the amount you are borrowing. For example, if you find yourself with $1,000 in additional costs and fees, your APR will account for $101,000. At a rate of 4%, that amount of money will coincide with an APR of 4.10%. You see, the APR takes all of the additional costs and fees it takes to acquire a loan, and not just the interest rate itself.

[ Looking for ways to start increasing your monthly cash flow? Register to attend our FREE real estate class to learn how to utilize passive income strategies in your local market! ]

What Is Interest Rate?

The interest rate of a loan is best explained as the amount lenders will charge a borrower to use their capital — expressed as a percentage, of course. In other words, the interest rate is essentially the price we all must pay to borrow money. Otherwise known as a nominal interest rate, the typical interest rate refers solely to the interest charged on a loan — no more, no less. Unlike its APR counterpart, interest rates don’t account for additional fees and costs; it’s literally the fee that has become synonymous with borrowing money.

Interest Rate Example

In an attempt to provide you with a useful interest rate example, let’s apply the 4% (just a hair under the average 30-year fixed-rate) interest rate I used above to a $205,100 (the median home value in the United States, according to Zillow). In this scenario, the borrower will have to pay the lender the original loan amount of $205,100 + (0.04 x $205,100), which comes out to a total of $213,304. As it turns out, 4% of $205,100 is $8,204, and if you add that to the original loan amount, you end up with $213,304.

What Is The Difference Between Interest Rate & APR?

The APR vs. interest rate conversation isn’t difficult to comprehend when you can break down each indicator — though subtle, the differentiating factors are easy to identify. In fact, while the two are objectively similar, their differences are enough to warrant your full attention. If for nothing else, it’s in your best interest to know everything you can about a loan and how much it’ll end up costing you in the long-run. And there’s only one way to do that: understand the difference between APR and interest rate — among other things.

If you are having a hard time separating the two, it helps if you understand one thing: the annual percentage rate is more than the interest rate. While the APR represents a combination of the original interest rate and any other costs incurred over the duration of the loan, the interest rate only represents the interest charged on a loan. Again, since the APR includes the interest rate (plus additional fees and costs), it tends to be higher.

“The main difference is that the interest rate calculates what your actual monthly payment will be,” says Sean O. McGeehan, a mortgage sales manager in Chicago. “The APR calculates the total cost of the loan. A consumer can use one or both to make apples-to-apples comparisons when shopping for loans.”

APR Vs. Interest Rate: Pros & Cons

The APR vs. interest rate debate is alive and well, and for good reason: the two share a lot of similarities. It is not hard to see why somebody would confuse one indicator for the other, or vice-versa. After all, annual percentage rates and interest rates are essentially two ways to describe a single financial concept. That said, there are inherent differences, and it may be easier to differentiate between the two by identifying each’s own pros and cons. Let’s take a look at the pros and cons of each and how they can help solve the APR vs. interest rate debate:

Comparing Mortgage Interest Rates & APRs Among Lenders

The best way to compare mortgage interest rates with annual percentage rates between lenders is to look at the standard loan estimates each provides, says Joe Zeibert, managing director of Global Mortgage Solutions at Nomis Solutions.

“The loan estimate is standard across all lenders,” says Zeibert, who helps top global lenders with mortgage pricing and strategy. “It’s a government document that will look the same.”

Therefore, comparing mortgage interest rates and annual percentage rates is as simple as looking at the government document provided by lenders.

“If (borrowers) wanted to compare apples to apples, they would compare the APR that one lender quoted them versus the APR that another lender quoted them,” says Zeibert.

Choosing Between APR And Interest Rate

Choosing between APR and interest rate comes down to one thing: the amount of time you expect to maintain the respective mortgage obligations. For example, those looking to stay in the same home for the length of a 30-year mortgage should seek out a loan with a low APR. That way, you’ll end up paying less for a home over the course of 30 years. However, those who aren’t spending as much time in one place may want to consider paying fewer fees upfront with higher interest rates, as the home’s total cost will be less in the initial years of the loan.

“If a consumer is only focused on getting the lowest monthly payment, they should focus on the interest rate,” McGeehan says. “But if the consumer is focused on the total cost of the loan, then they can use the APR as a tool to compare the total cost of two loans.”

The differences between annual percentage rates and interest rates are minimal, but they are important nonetheless. Those who don’t have a firm grasp of what these indicators mean for borrowing money could find themselves between a rock and a hard place. That said, it’s those that know exactly what interest rates and APRs are that stand to realize more success. If for nothing else, these two rates are small but important factors for determining overhead costs.

Summary

There is literally no answer to who will win the APR vs. interest rate conversation, but it stands to reason that those that know both sides are ahead of those that don’t. That said, are you aware of the differences that exist between each? Have you ever found yourself wondering which indicator is better for you to consider? Whatever the case may be, feel free to let us know in the comments below.

Ready to start taking advantage of the current opportunities in the real estate market?

Click the banner below to take a 90-minute online training class and get started learning how to invest in today’s real estate market!