Where do you get your capital to start investing in real estate? Hard Money lenders can get you the capital you need in 24 hours. Jeffrey Rutkowski’s guest today is none other than the Co-Founder of Fortune Builders and CT Homes, Paul Esajian. Paul discusses with Jeffrey that it’s not the cost that matters, it’s the availability. You can either save that cost and make no money or, you can pay to play! Paul went from bartending to billionaire through the methods he’ll share in this episode. Tune in, be resolute, and get that capital!

—

Listen to the podcast here:

The Best Source To Get Your Capital With Paul Esajian, CT Homes Founder

We’re going to be talking with a man who went from a bartender to a billion dollars owned in real estate assets. This story is going to leave you inspired but we’re also going to leave you educated because we’re going to be getting into things like private money, what is it? How to raise it? Wait until you learn about what he has to say about big banks and borrowing money there. Before we get into the episode, we’re going to kick it off with our word of the week segment. Our word of the week segment is private money versus hard money. What are they? What are the main differences? I want to give you a high-level overview. As we talk to our guest, you get the most out of it and you’re tracking right along with us.

Get Your Capital: People who’ve made money either made it in real estate or park it in real estate.

Let’s start with hard money. Hard money is loaned to you by institutions or businesses in the business of loaning money to real estate investors on distressed assets like we’re making offers on. Assets need to be wholesaled, assets that need to be rehabbed, assets that you’re going to rehab and buy and hold. Every hard money lender is going to be a little bit different. Typically, they like to run credit checks on you, not that they won’t loan you money if your credit is bad but they’d like to see your current financial standing. Their main focus is the asset that you’re bringing them. What is it worth in its current condition? How much are the renovations going to cost? More importantly, how much is that asset going to be worth after you renovate it?

They’ll loan you anywhere from 100% of your acquisition price to about 80% of your renovation cost. Some of them will do the exact opposite. They’ll loan you 80% of your acquisition cost and 100% of your rehab costs. It’s their business. They call the shots. They all have different terms and conditions. As you meet multiple hard money lenders in your market, you’ll recognize that. What’s powerful about hard money and why we should be interested as real estate investors is its capital that’s available to us quickly. We could close our deals in 7, 10, 14 days, whatever your hard money lender can deliver for you.

Private money would be similar in concept but different in terms of who’s loaning you the money and the conditions that go along with it. I like to refer to private money lending as relationship lending. They’re not necessarily in the business of loaning you money. They could be coworkers, school teachers, an attorney or they could be another real estate investor that wants to grow their money at a higher rate of return than the bank is offering to them, CDs or mutual funds, whatever it may be. What we love about private money is the rates and fees will be lower than hard money. They’ll cover 100% of the deal as well.

Life will do what it needs to do for you.

With hard money lenders, sometimes it’s 100% of acquisitions, a certain percentage of renovation or vice versa. While the private money, if you structure the relationship right, can give you 100% of acquisition, carrying cost, renovation costs, and holding costs. You’re doing the deal with no money out of pocket. When you’re doing a deal with no money out of pocket, your return on your money is infinite. We love that, as real estate investors, an infinite return on our money.

Which one is better? Which one do we want? We want both of them. Why do we want both of them? “Why would I use hard money, Jeff, if private money could be less expensive for me?” That’s a great question. When it comes to raising money for your deals, the underlying principle is that it’s not the cost of the capital. It’s not the cost of the money that matters. It is the availability of that capital. Maybe you have $1 million set up in private money but you have that deployed. You have that working on multiple deals right now and another great deal hits your desk.

Your only option is hard money and you’re going to have to pay high fees and high interest on that. After paying the high fees and the high interest, you’re going to make $30,000, $40,000 or maybe $50,000 on the deal. Do you do the deal? If you’d like to make $30,000, $40,000 or $50,000, you do the deal. That’s what it’s about. It’s not about the cost. It is about availability. That is our Word of the Week segment.

We have a legend with us. Bartender to billionaire in assets, Mr. Paul Esajian. Paul is the owner and founder of multiple multimillion-dollar companies. In the real estate game, he has flipped, rehabbed, renovated over 1,500 properties in his career. He surpassed over $1 billion in real estate owned. He’s also an Educator and Owner of Fortune Builders. He is the host and the sponsor of this show. Without this man, this show is not possible. We are excited to have Mr. Paul Esajian with us. Let’s get into it.

—

It is truly an honor to have Mr. Paul Esajian with us here on the show. For those of you that don’t know Paul, he owns many companies. He’s a serial entrepreneur. He has a little company called CT Homes. They’ve flipped about only 1,500 homes and counting, 100 homes a year like Clockwork. Paul, you’re going to cross $1 billion in commercial assets owned. First of all, congratulations. That is incredible. He’s also a co-owner of a company called Fortune Builders, which is the owner of this show as well that teaches and trains over 30,000 students all across the United States. It’s an honor to have you here. I want to get started with this. I remember being new to real estate, reading some books and hearing stories of people that have accomplished things, it seemed unobtainable, 1,500 homes, $1 billion in assets. You started as a bartender.

I love my bartender’s story. I love teaching and sharing it. As I share all the time, I didn’t come from a real estate family. Real estate wasn’t given to me. It was the sheer observation that we all have, frankly. If your reading this, you realized two things. People who’ve made money either made it in real estate or parked it in real estate. It’s 1 of the 2. You can’t point to someone with a large amount of money and doesn’t leverage real estate in one way or the other. That was our observation. Dan and I when we were saying, “What are we going to do with ourselves?” Fresno, California, is the second most visited city outside of Anaheim Disneyland in California. Do you know that? Maybe that’s not true but at least that’s what I like to think. It’s God’s country there. It’s beautiful.

Is Bridgeport number three?

Bridgeport is probably number three. I grew up in Fresno. I got an Economics degree at UC Davis up North in California. I ended up in New York City. I should share the story. It’s good to learn about the journey of different people. This stat on the commercial, Assets Under Management. That’s one bucket of our assets where we’ve crossed $1 billion of bought and owned commercial assets across the country. It’s fun when you can use an M at the end of your numbers but when you can use B, that’s even more fun.

Can we get a T?

Get Your Capital: One thing we don’t have to be bashful about is traditional education. It doesn’t set up everybody for the economics of living life.

I don’t know. We’ll see. We’re still doing this show in a couple of years. I value my traditional education. One thing, as I sit here now, is that your traditional education, business and real estate education are two different things. A lot of people believe or think or don’t understand that after your traditional education stops, junior high, high school, college, they think that you’re done learning. That’s the start.

One thing we do know is traditional education doesn’t set up everybody for the economics of living life, how to make, save and keep the money. I remember going to an interview on campus in my last year in college. The night before, a friend came into town and it was Taco Tuesday. I woke up and was a little crusty from the night before. This was spring in Northern California. I remember walking to the nondescript campus building. This interview is with Pepsi to drive around sales for Pepsi.

I go into this small room. It’s probably about the size of the booth we’re doing the show in. I’m getting interviewed. I had to wait in line and there are other kids in their cheap suits. We’re in college. There’s a window behind the person interviewing me. I remember not during that interview but leading up to this. I don’t understand or buy into the story. I go to school, I get a degree and I get a job for $35,000. Next year, I get a raise of $37,500. Year 3 or 4, I’m at $40,000 or $45,000. Thirty years later, I can retire and do what I want.

It never resonated with me. I had some entrepreneurs in the family, my dad, his dad and whatnot. I was always thinking, “I don’t see that I’m going to reach my goals of getting a job.” There’s nothing wrong with a job. I like working. I remember sitting in that interview thinking that I’m not completely buying in, answering questions. Last night was Taco Tuesday, I’m getting interviewed, it’s early in the morning. All of a sudden, the interviewer snaps his fingers and he goes, “Are you listening to me?” I realized I was looking out the window on that spring morning with the dew, the water tower, birds were flying by. I wasn’t listening to him. I didn’t get the job and I’m glad I didn’t.

It’s one of those things that life is going to do exactly what it needs to do for you. I believe in that wholeheartedly. The reason I also believe in everything that happens to you happens for a reason because if that’s not true, what else you’re going to subscribe to? All I remember is knowing that I love New York City. I’d done two visits to that point. I got my degree. Long story short, I ended up in New York City without a job. I believe life is like this 100%. We don’t always know what we want to do but we do know what we don’t want to do.

Life’s like a hallway and it’s a series of doors. When you know that that door, you don’t want to go in, you shut it. There are then a couple more left open. You keep walking. Sometimes you go into the door and come back out and shut it to learn that lesson, “That’s not what I want to do or where I want to spend time.” That could be a week, a month or a couple of years. People reading this are in different stages, “I’m shutting a few doors and there are some new opportunities I want to learn and be a part of. It’s scary. I don’t have the answers on which door and how to get there and how to achieve it but I truly believe that.” At that time, a few doors I didn’t want to go through, which is a traditional job right out of college.

I moved to New York City in August of 2001. I had a 500 square foot apartment with my college buddy that I wrestled with. My share of the rent was $1,000 a month. It’s 500 square feet in 2001. It’s $2,000 in total rent. I remember I was sitting in the great city of Fresno, California. My buddy that I was getting this apartment with, who was already in New York City, said, “I found an apartment. The best thing about it is that your room has a closet.” I’m sitting in California. I got a closet in Fresno and I didn’t know I wasn’t supposed to not have a closet in New York. I moved to New York City and this is back when it was cheaper to get a round trip ticket than one way.

I packed my life in a duffel bag. I like this story because I’ve had versions of this story where you come to a crossroads and you have to be honest. It’s overcoming fear like, “I don’t know what I’m going to do or want to do but I do know what I don’t want to do.” This was one of those moments where you had to step across the line and say, “I’m going to take a risk.” You have all your friends and family trying to support you but they’re doubting you. You have the people who aren’t your friends and family and they’re telling you you’re stupid. This is the analogy for all of you reading says, “I’m going to get into real estate.” It’s the same thing. The people that love you, they’re supporting you but it’s not their fault. They are fear-based, too.

I remember that being one of the first bigger experiences. I packed my life in a duffel bag. I bought a round-trip ticket that I didn’t come back on. I got there in August 2001. I’m in a 500-square-foot apartment. I don’t have a job. I don’t know if anyone’s done the math here but in August 2001 in New York City, a month later was September 11. The time between those 30 days, I was interviewing. I got a headhunter. I’d never lived on the East Coast and I had my cheap black suit from Mervyn’s. I don’t know if anyone knows Mervyn’s.

Nobody knows what’s better for you than yourself.

Men’s Wearhouse was high. I couldn’t afford that. Mervyn’s was the West Coast cheaper retail store. I’m walking around New York City in August interviewing and sweating my ass off and I’m like, “This is miserable.” I go into this office building that’s 100 stories or more or less and I’d sit in the same interview. You’re walking by everybody in their cubicles. I had the same thing, I’m doing the interview and I’m thinking to myself, “I hope I don’t get this job.” It’s the lessons I already knew, which was I know what I don’t want to do but society’s pressure, society’s talk tracks, it’s hard to have enough conviction to say, “That’s not for me.” I was still going through that process.

We’re trained as little kids to work hard in school, get good grades, get into a good college and get a job.

That might be a great track for some people. I knew it wasn’t for me. I guarantee the people reading here have some version of that not being their perfect roadmap but it’s still hard. I’m sharing that you’re going to have to exercise that muscle multiple times in the process. I didn’t get any good job offerings but I had to pay rent. I live in New York City. I don’t have a car. I walked around the neighborhood and saw a help wanted at a sandwich shop for a cash register. I got to pay rent. I go in there. The manager lets me train for a half-day on that cash register. Jeff, no one works the cash register as I would. I was crushing it.

It doesn’t surprise me. You love money.

I like counting, being organized and pluses and minuses. I do that half-day. After I get done training, she calls me into the back office and says, “You did great.” I said, “Thanks.” She said, “I want to ask you a few more questions and then we can rock and roll.” I’m like, “Fantastic.” She’s like, “Tell me a few of your goals here.” I said, “I want to get this job so I can make some money to find a better job.” I’m a kid from Fresno, California. I used to work at a raisin packing house in Fresno so maybe it was a little bit of a country bumpkin attitude or naivety. She looked at me and said, “I don’t want to train another cash register.” I said, “Train?” I didn’t get the job. This story is leading up to the bartender but there are lessons along the way. I’m like, “Lesson learned.” This is for everyone reading too. There are times when you need to market yourself to people that don’t know about you but there are some things you don’t need to market. I shouldn’t have marketed the fact that I was using that as a stepping stone.

It’s like, “I got to get a job. I got to get something to pay the monthly rent.“ The pressure was on. This is that August 2001. I walked by this bar-restaurant in Soho and I walk in and I say, “I’d like to interview.” They said, “Every Thursday is when we do our interviews.” It’s a large restaurant, bar, bakery, everything else. The restaurant’s name is Balthazar. It’s still there. It’s like an institution. I go back Thursday in my cheap suit and I never worked for any material type at a restaurant. I get the application and I check every box, “What are you interviewing for? Waiter? Cook? Bartender? Barback?” I didn’t even know what a Barback was and I’m checking these things.

Finally, I get called at the little cafe table in the bar area and the gal who’s doing the interview, as I walk up, I see her sizing me up. I sit down and she says to me one of the first questions, “Can you lift boxes?” I said, “I can lift boxes.” She asked a few more questions and she said, “Our barback left for some time. Would you like to barback at this restaurant?” I leaned in and I looked her in the eye and said, “I’ve wanted to barback at this restaurant since I was born. It is my life’s dream.” I’m a quick learner and I got the job. I ended up being hired as a barback.

Once I got to work the first day, I’d ask people, “What does a barback do?” It’s the busboy to the bar. What I learned is that it happened to be the hardest physically, mentally and emotionally job I’ve ever had because there was a basement with two stairs and a hallway. I’ll call it 50 to 75 yards. Multiple times throughout the shift, I’m going down the stairs, the hallway and getting boxes of wine, beer. I’m restocking and I’m bussing the bar. All this stuff was hard. Long story short, I climbed the corporate ladder and became a bartender.

Coming full circle with this story. I love living in New York City. It’s a great place. I learned many lessons. I loved working in a restaurant. It’s fast-paced. You’re learning how to deal with people. Especially behind the bar, you’re learning psychology and you’re a psychiatrist. You see people deteriorate as they keep drinking, which is fun and interesting. I was about two years into it. At that time, I was working there when September 11 happened. About two years into it, the fun started to wear off a little bit and I said, “This has been good. I’m glad I wasn’t stuck in a cubicle but this can’t be the rest of my life.”

Real estate was always on my mind and calling my good friend, Than, we said, “What are we going to do? We got to do real estate.” That’s the name of the game. It was 2004 when I quit the bartending job. At the midpoint in 2003, we went and got every book and got any type of training. Back then, it wasn’t webinars. It was teleconference calls. Than was reading a book and at the back of it, there was this, “Here’s a discount for our five-day real estate training in Redding, California, Fixer Jay’s.” We flew all the way across the country for that education. It was like $5,000 or $4,000. JD and I stayed at Motel 6. That’s the first time I remember being in a hotel room, you could put quarters in and the bed would shake.

Tell me you didn’t do that.

I did because it was pretty interesting. I happened to be sharing the bed with my brother so it wasn’t exciting or anything.

I hope not.

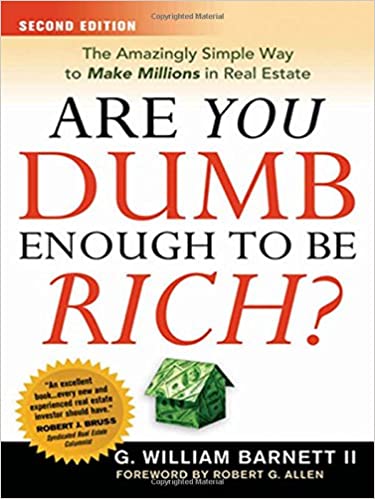

That was an important process for me. I enjoyed that period. After two years, one of those doors shut and said, “I don’t want to stay up till 2:00 AM and then another two more hours to break down the bar. This can’t be my lifestyle to reach the personal and financial goals that I want for my life.” That’s when I had to do another big step. A couple of months before I quit, I remember telling my bar manager and then my co-workers, “I’m going to stop working.” December 2003 would be my last month. I’d walk in with my books. One of the books that I read that I can still remember vividly, the messages and the visuals the book gave me Are You Dumb Enough to Be Rich by William Barnett.

I remember that book.

Get Your Capital: To improve your finances and your real estate business, you have to educate your way out.

I remember walking into the restaurant during my shift. We had this downstairs with the locker where you get changed with the co-workers. My co-workers love that title because they were teasing the crap out of me. They didn’t believe I could do anything. They were my friends but they’re like, “This guy’s crazy. Is he out of his mind?” In 2003, 2004, the same things were said to me that the people are going to say to everyone reading when they go into real estate. At that time, the people that I knew were saying, “Are you crazy? Now’s not the time to get into real estate. Now’s not a good real estate market. Now it’s gone up too much. It’s coming down too much. It’s too much this or too much that.” I can tell you that’s a universal message at any time when you start from the people that you know.

The thing that tested me is that I have a great family and I’m thankful for my big Armenian family. My parents are great and I remember calling my mom. I was making $50,000 in cash or maybe more. $60,000 a year in these two years I was bartending and that was great. My mom was happy I was providing for myself and I called my mom I said, “Mom, I’m going to quit my bartending job and I’m going to move to New Haven and start a real estate business with Than.” She says, “You have such a good job. Are you sure you want to do that?” I know my mom loves me but when she’s putting a chink in my armor on the decision, that’s when you understand nobody knows what’s better for you than yourself.

I found it, too. I experienced the same thing. How many times that you get to tell early on, “It’s time to get a real job.” I remember hearing that over and over. I found that most people around us are not comfortable with what they’re doing but they’re afraid to take that step. It makes them look at themselves and then take it out on you. I agree.

That’s the story of the longer story. There was a ton of lessons along the way, from my traditional education to when we started real estate. One of the first lessons I learned when I started real estate is that education is the key. I can tell you the first deal that we bought. I’m in New York City and my buddy and business partner happened to be in New Haven. I would get on the Metro-North and Grand Central. Correct me if I’m wrong but I do believe it’s the last stop or one of the last stops in New Haven on the Metro-North from that line.

I believe it is.

I don’t’ have a car. I’m living in New York City. I’m working at the bar during the week and weekend. I’d get on the Metro-North. I go to New Haven. Than would pick me up or we had this one real estate agent and this is how we learned the market there in New Haven. I was like, “We’re going to do real estate. We need to buy and own stuff for cashflow.” It’s what we read and learned. There’s also this idea of rehabbing and flipping houses for profit and all that. Our first thing was, “Let’s buy some rentals.” For 3 to 4 months, that was the routine, back and forth on the Metro-North, get off at New Haven and then go around different neighborhoods in New Haven. None of which were too fancy.

It’s driving for dollars.

The first rental house that we bought, 876 Elm Street. If anyone knows New Haven, it’s not far from the Yale campus. It’s a three-family house. It’s approximately $186,000 I want to say. We got a conventional loan. We talked to a mortgage broker. Than and I pulled the money that we had saved and put down the down payment. That was the first rental house that we bought. It was our first investment piece of real estate. We bought that and then within a month, one more three family 79 – 81 Blake’s. You never forget your first year. These were two rentals and then two things came to a huge realization. We had no more money because we put it down on traditional financing as a down payment. We’re like, “What do we do now? How do we keep “doing real estate” with no money?” Once we closed on these rental properties, we started to learn everything we didn’t know, deferred maintenance, tenants don’t always pay, your spreadsheet and your tenants don’t always agree.

We were supposed to cashflow $1,000 a month but I learned that was not a promise or a given. We had to start putting money and time into these houses. You can’t work your way out of that. You can’t keep fixing the house and spending time with the tenants if you’re going to improve your lot financially. In your real estate business, you have to educate your way out. I remember this one experience at 876 Elm Street, the tenant calls me and says, “My toilet is clogged. The sink is clogged.” Something in the third-floor bathroom wasn’t working, the toilet or sink or maybe both for that matter.

I bought this toolbox from Lowe’s and also we bought this van, Chevy G20. It was this gray gunmetal van, no windows with a sliding door. I jumped in the van. I drive over there with my toolbox. I go up to the third floor and I get in the bathroom. The tenant points out the problem. I opened the toolbox, I look at the problem, I look at my tools and then I realize I have no idea what to do. I call the handyman and spend money to get it fixed.

The point is that I remember that experience. What was more important on that day was a Saturday. My good friend and business partner, Than, was at a one-day real estate class learning how to flip houses. He had to spend money and time. I remember talking to him. I’m saying, “We need to spend more time at these houses and fix them up ourselves to save money.” He was saying, “No. I don’t think that’s the answer. Here’s what I learned. We need to rehab houses. We need to market for deals and not buy them through realtors. We need to do creative financing. I learned all these introductory items today. We don’t need to spend more time at the shitty houses we already own. We need to learn how to get rehab, buy, fix, sell it and get a profit so we have money.” It was a mindset shift there. That’s hard because we were all out of money. What we were leveraging for education was credit. That was a paradigm shift too. That was the first experience. Usually, when people ask me when I get interviewed about our first deal, I talk about the first rehab deal we bought.

That’s what I thought it was.

I don’t always give that precursor but that was an important precursor because here we were, we bought these rentals with conventional financing. Whatever money we’d save, we put down. Now we had no options to do anything because we’re fresh out of cash so that set us on the educational journey. I remember being on the floor of our four-story brownstone walk-up in New Haven huddled around a phone, listening to a teleconference call and anyone who would allow us to be on these real estate conference calls to learn.

Auctions and foreclosures in New Haven happened in front of the house. They’re posted the week before in the paper. You know this. You’re from Connecticut. We started researching all the auctions on the weekends. We would take properties from the paper. We do as much due diligence as we could and then we’d split up. Than would get a bank check with whatever little money we had. You had to show up at the bank check. I get a bank check and then he’d have 3, 4 houses. I’d have 3, 4 houses or so and then we’d split up. We go to the Saturday morning auction. We’d have a max bid and see if we could win a property. This was how we started.

Why were we doing this? It’s because we wanted to be in real estate but we’re out of money so you have to rehab, meaning flip properties and wholesale deals to get money back immediately. I remember going to my house. I didn’t win anything. This is Saturday. At the second half of Saturday, I called Than and he’s done with his auctions. I’m like, “Than, how did it go?” A bunch of kids from Fresno run around New Haven trying to buy properties. He said, “I won the bid.” He’s excited and I’m excited. I’m like, “Awesome.” We’re in all this excitement.

I asked the first logical question, I said, “How much did we get it for?” He said, “$75,000.” I’m like, “This is great.” It sounded like it was great to him. I asked the next logical question, “How are we going to pay for it?” He’s like, “I don’t know.” That’s when a little bit of the wait, a little bit of the how we’re going to do this happen. I remember we didn’t talk too much on the phone after that. We got off the phone. We’re single guys at the time living together in this four-story walk-up brownstone in New Haven, Connecticut. We go back. I remember because it’s the second half of the day, we’re like, “We’re going to have to dial for dollars.” That’s exactly what we did.

It’s not a true dream vision if you’re not willing to do anything and everything it takes to do.

We were calling all our friends. The first investor that I was able to get into the deal was my older brother, JD. He’s sitting in Fresno, California. I got him for $10,000. He was the first one. You’re probably going to interview him. When you talk to him, he might have a little amnesia and thinks I still owe him $10,000. Tell him he’s paid off in full. The way an auction works in any state whether it’s in front of the courthouse or front of the house, you give your bank check. This was about a $7,000 bank check and then you get 30 days to close on the property. This is not like, “You didn’t figure out how to get the money. Here’s your $7,000 back.” It’s, “You didn’t figure out how to close. We keep your $7,000. Good luck next time.” There’s real pressure. We had let go of that bank check. The game is on.

We call our friends and family and we had two rooms next to each other in this four-story walk-up. At the time, our bedroom also doubled as our office. I remember because we were trying to clean up this place so my mattress was on the floor. There was a bucket of a compound and there was some plastic. We were in the middle of a work zone. They’re trying to make this place at least halfway decent. He’s calling everybody he knows. I’m calling everybody I know. Eventually, we do good. We call through our cell phone and then we convene back in the hallway, which is 1 step out and 2 steps and we’re face to face. It’s not a big place. We’re short about $25,000, $30,000.

We’re getting there but it’s getting depressing now. Remember, I made this big decision to leave a job that was paying me. It doesn’t matter what the job is. I had “job security.” I was making money. Now I’m about to lose $7,000. I own these two rentals that are not that great. I got tenants not paying and work that needs to be done. This is running through my mind. We go back to our rooms and then all of a sudden I hear Than on the phone. He comes and gets excited. He runs over to my room, which means he takes one step from his room to get in front of my room.

Than, if you’ve ever seen Seinfeld, he has the George Costanza wallet. Every card he’s ever gotten since high school is this huge. It’s like this thick wall. He’s like, “I called my credit card. I got $7,500 advanced. I’m excited and that’s amazing.” He’s excited and I’m excited. Your friends or family that you’ve known your whole life, do you know when they can look at you and have a full conversation without saying anything? He’s holding this huge wallet and he looks at me as if to say, “It’s your turn.” I’m sitting on the floor on this mattress, there’s a bucket of a compound, there is work dust, there’s plastic. I look at him and I remember my first immediate response was, “No way. I quit my job. I moved from New York City to go all New Haven here. It’s not quite the same. $7,000 of our last dollars is on the line. The one thing I have, Than, is my credit. I’m not going to screw that up. This is how I’ve been trained, to have good credit.” I say that with conviction. With one look, Than takes his eyes and he scrolls the room that I’m in. It’s not big. He comes back in eye contact with me, he’s like, “How’s that credit working out for you now?”

Do you know when they say your life flashes before your eyes? At that moment, it hit me pretty hard because I thought about everything from that point to now. I could see if I gave up, if I failed and if I failed without exhausting my resources, without burning the boats, without doing everything I could. Also, going back to that restaurant bar in New York City with my tail between my legs and saying, “Could I have a job?” They’d have taken me back but I would not have liked it at all.

I visualized that whole thing and all the people telling me, “I told you so. You should have never done it.” At that moment, I realized it’s not a true dream, vision or goal if you’re not willing to do anything and everything it takes to do. That doesn’t mean the lesson isn’t to do what we did to get started. Everyone’s in different stages. If you’re not willing to exhaust the tools and the resources and put in the time and take the risk then maybe it wasn’t what you should be doing anyhow. I knew right then in there that was my lesson.

Long story short, we got it. We pulled credit. We got friends and family. We closed on that property and that was our first rehab. In 32 Main Street, New Haven, Connecticut, we bought it for $75,000. We estimated that it needed $50,000 or maybe it was $30,000. This is 2004 when we got it. I remember thinking, “That’s enough rehab because that should be enough rehab for anything.” We went over budget over the timeline. We screwed everything up. There were a lot of lessons learned.

Our target profit, we didn’t make. We made about $27,000 by screwing everything up. Through what we were learning, having that experience, we had a few rentals. To get $27,000 and it was less than six months, as most money I’d ever been able to see and create on my own and it was like, “How do we do this not once every six months? Not a couple of times a year but a couple of times every quarter. How do we get multiple going?” That was the drug that hooked us. From there, the rest is history. That’s the first deal.

That’s an amazing story on the first deal. I want to get into how you’re funding deals today. I want you to teach the audience a little bit about private money because I know that’s going to be part of the story. Before we get into that, though, speaking of getting started and getting your first deal, we have a real estate class coming up that Paul and his business partner, Than, teaches here at Fortune Builders. It’s a one-day virtual event.

If you’re reading this, you’re learning about Paul’s story and you know there’s more out there for you than what you’re currently living and you know that you’ve always had a desire to learn about real estate. Whether it’s getting into a full-time or doing a couple of deals a year around a job you love. I would highly recommend this class. It’s where I got started back in 2007. It was a paradigm shift in my life where everything changed. It’s been great since. If you’re interested in that, go to FortuneBuildersShow.com. It’s easy to sign up for the class. It’s a free one-day event. Usually, we don’t have the actual person that will teach the class here in the booth. Why is it something somebody should go to? What do they experience?

What we do at Fortune Builders, our education company is we introduce, share and teach how we successfully do this business, how we find deals, acquire deals and raise capital. These are all the questions. When you say, “I want to get into real estate.” Immediately after that, it’s like, “Where do I get the money? How do I find the deals? How do I execute the rehab?” This class is amazing because it introduces you to the fundamental concepts of what we do daily here at CT Homes. That’s our residential redevelopment company. We’ve sold over $40 million of renovated single-family, 1 to 4-unit, what we call residential real estate each year. We’re at a high level in this market.

We’re sharing and teaching what’s working and what they need to know to get started and what they need to know to keep leaning into the real estate journey. I love that training because we cover a little bit of everything in a day. We don’t take one topic and put you to sleep but it’s like, “Here’s how you find the deals. Here’s why real estate is valuable and important for some tax reasons.” We go through some different IRS-sponsored codes that people don’t realize but are given to us as real estate investors to keep more of the money we make.

We talk about the seven-stage rehab process that we’ve perfected for over seventeen years in our CT Homes Residential Redevelopment Company and the fundamentals of that system, how we use six critical documents with each contractor to manage the timeline and budget. Also, selling them and moving into commercial deals too. We love residential real estate. We love commercial real estate. We love real estate because you make a lot of money. That’s a great place to get started so spend time and kick off your educational journey or, for some of you, advance it.

I highly recommend that class. FortuneBuildersShow.com is where you’ll get that information. We go from the first deal of scrambling, raising money from credit cards, friends and family, whatever you do to make it happen. What are some of the top ways that you are funding your deals?

It’s a great question and it’s the fundamental question we always get asked when someone is interested in real estate. They say, “How do I get the money? We all come to the real estate table with either a little money, no money. This is a universal problem that we all need to solve. Some of our successful investor students had a great career and they’re a little older. They have some money. At some point, I don’t care who you are, you start with some money and it runs out if you don’t leverage the principles that we’re going to talk about and teach in our training in raising capital for deals.

Let’s break it down. There are three areas that people either know or don’t know that you can get money for your real estate deals. You can get it from a conventional bank, Bank of America, Wells Fargo, Chase, etc. That’s what I mean by a conventional bank or your local, regional bank. You can get it from what we call rehab lenders or hard money lenders. These are businesses that are specifically created and designed to find us, meaning me and you are looking to buy crappy properties, fix them and sell them. They also know the risk so they charge an appropriate interest rate and cost to that money.

The third area, which not everybody understands, has heard of or gets how it works, is private lenders. Private lenders can be anyone you educate to be a lender to your next real estate deal. There are three big buckets. I’m going to take one away right now and it’s the conventional banks. Bank of America is not going to loan you money. They weren’t going to loan us money on 32 Main Street that was vacant, boarded up, had a layer of crap, King Cobra bottles, drug paraphernalia. It was a squatter house. Because it was not livable, conventional financing or any financing from them was not going to be available. They’re off the table.

They’re slow even if it was available.

Are You Dumb Enough to Be Rich?: The Amazingly Simple Way to Make Millions in Real Estate

For everyone reading, if you’re banking at a large national bank, stop. You got to get a relationship banker. You got to go to a local, regional community bank and start your personal and business banking relationship there. It’ll pay off in a year or now or a year or two from now. I won’t go long on that. I teach people that if you don’t have an actual banking relationship, you don’t know what you’re missing. You can’t have that at the big banks. I have accounts at Bank of America, Wells Fargo, Chase, US Bank, all of them. That’s not where I brainstorm and solve solutions with my banker. That banker is at a local, regional bank here in San Diego or the Central Valley. I have a couple. That’s one lesson I’d love for folks to learn, listen and write down and hopefully grab on to.

Now we’re left with rehab, hard money, lenders and then private money. I’m going to say this one thing and for some of you, it should be an a-ha moment because you’re wondering, “How do I get money for the house that I’m going to try to buy and rehab?” Maybe your market is a $200,000 purchase in rehab. Maybe it’s like in San Diego. It’s $600,000 or more purchase and rehab capital needed. Your rehab lender, hard money lender and I’ll teach what I mean when I use those two different words. They’re in the business of qualifying you.

Our Fortune Builder investors students have a seven-stage rehab process. They’re educating the lender. They show an example of the six critical documents where they have an independent contractor agreement, which has a timeline, penalties and bonuses. They can manage the timeline and budget. They have a payment schedule tied to benchmarks and milestones of the rehab. They have a scope of work that itemizes out everything. They’re going to put in that house before they start and lien waivers and insurance indemnification agreements. That’s part of the six critical documents. They show that to a lender because they show they have a business, a business plan and business systems. When you do that, if you present your deal to a hard money lender or rehab lender, within 24 hours you can get 75% plus or minus of the capital stack you need to buy your house. Think about that.

If you’re reading this and you’re waiting to know the big answer on how you get money for your next rehab deal or your first, there’s 75% or sometimes more of the money you needed. People are like, “I don’t know. I’ve told it’s expensive to borrow from hard money lenders or rehab lenders and all this.” It’s not the cost of capital that matters, it’s the access to capital. When you’re making an average profit in New Haven, Connecticut on about $30,000, are you paying 15% and 5 points on money? Who cares?

Let me jump in there. I want to say that again because I hear many people get hung up on this point. What Paul said is not the cost of the capital. It’s the availability. I got started with you guys in 2007. I won’t get into it now but some of you guys know my story. I had a bankruptcy 6, 12 months prior, something like that. The first deal, all I had available was the hard money at 13.99% and 5 points. A point is 1% of what you’re borrowing. I remember, “That’s ridiculous. I’m not paying that money.” My coach exactly said what you said. He’s like, “You can borrow that money and can make $50,000 or you can not borrow that money and not make $50,000.”

You can “save” that cost and make no money or you can pay to play. That’s another big paradigm shift for people getting into this business. It’s not the cost of capital. It’s the access to capital. There’s 75% of your capital stack. You’re asking, “Where do I get the rest of it if I don’t have any money?” The rest of it would be from what we call our private lender opportunity. This is where, in a lot of scenarios, you’re teaching, educating and training your friends, family, co-workers or acquaintances on how they can be the bank to your next deal.

I had done teaching our investor students in a two-day training on how to raise all the money you need for your deals. There are a few things that I teach. It’s not hard once you get an education. People outside reading to this podcast or outside of our network, Jeff, are looking to make money. People like making money. What are their options? They have a CD account at the bank. That’s conservative. They think, “I won’t lose. I can make an interest there.”

They have the stock market. The stock market is great but the stock market average is 8% or 9% if you stay in it for 30 years because of the ups and downs. A lot of people don’t have the stomach to lose money and make money throughout the period they’re waiting to retire. That’s nerve-racking for some people. You got your bank. You got your stock market. As an everyday person who’s got a good job, you’re busy with your family, what options do you have?

Here, we give people. We educate people. How would you like to be the bank? Here’s the first thing I teach people and I’ll share this little golden nugget. A lot of times, I meet someone and I start explaining the private lender opportunity and they ask me, “What does that mean? What is private lending?” I share with them, “Remember when you bought your house?” They say, “Yeah.” I said, “Remember when you signed a promissory note, all the terms in which you promised to pay the bank back over the course of that 30-year mortgage?” They said, “Yeah.” I said, “Remember, you also signed a trust deed or mortgage deed depending on what state you’re in that got filed on the land records. When you sold that property, you had to pay the bank back first before you touched any of your own money.” They said, “I remember that.”

I said, “Remember right before closing, they said, ‘The bank wants to confirm and see that they were added to your insurance as a loss payee.’” They said, “I remember those three things.” I said, “You get to now be the bank to my next real estate deal. Here’s the best part. Instead of waiting 30 years to get paid back, we pay you back in twelve months or less. Even better, the bank charges you maybe 4% or 5%. We give a double-digit 10% simple interest rate of return on your private capital. You get all the same promissory note, security instrument, mortgagee, trust deed on title added to our insurance. How would you like to be the bank?” Usually, you lighten up. You’re like, “I’m in.”

Oftentimes, people are like, “I feel safer and I’m going to keep my money in the bank because I don’t want to take the risk.” I live by a few principles that I’ve learned throughout my life and my business life. People lose more money by indecision than by not making a decision. I get hit with that all the time, like, “It’s better. It’s safer. I’m better off.” Let’s break that down. This segment is talking about how we raise money for our real estate deals but you have to understand the economics of money. You have to understand the policy of money, fiscal policy and how money works.

It’s not the cost of capital that matters. It’s the access to capital.

On average, inflation is about 3% a year. Let’s talk about this for a minute. Another paradigm shift. This is me hitting everybody over the head if they don’t realize this already. If you’ve got money sitting in a bank account or a savings account, that sucks. Get it out. You’re like, “That’s BS, Paul. What are you trying to do? What are you trying to tell me? Are you trying to get me to give me your money?” I’m like, “No.”

If inflation is 3% and let’s say for the last three years you’ve had your money, your nest egg, in your checking account, savings account or a CD. The average interest rate on a savings account is 1% plus or minus. That might be high. The Fed rate for the cost of capital is lower than that. LIBOR and SOFR are almost 0% as we speak. You’re maybe making 1% of your savings account. Maybe you got a CD for 12 months or 24 months or 6 months and maybe you have a little bit more, 1.5 or something. In your checking account, you might have no interest rate. Let’s say you’re in your savings or checking. Your dollar is losing 3% a year. In this arbitrage, if it’s in your savings, it’s 2% or 0.5%. The value of your dollar is going down.

Thank goodness, coming out of a pandemic. It affected everybody. It affected the whole world. It affected business. We’re all still learning all the effects. What did our government do and most governments to help get us out of this pandemic financially? A lot of things but they said, “We got to push money into the economy.” They started PPP funds. They gave businesses money, which was great. That helped. Our government is not sitting on extra money. When they need more money, what do they do, Jeff?

They print it.

It’s supply and demand. When you have more supply, the demand and the value goes down. Our administration is looking to do more of it. I’m not saying that’s good or bad. It’s probably helpful. As more money gets printed, as more money gets pushed out from the government, the cost of your dollar is at a higher risk of losing value. I’m tying it back. We’re talking about raising money and private lenders. When I get that private lender that says, “My money is safer in the bank account.” I tell them, “Each year, inflation on average being 3%, the value of your dollar is eroding by 3%. Here’s worse that I want you to understand Mr. or Mrs. Private Lender. Do you know how a bank gets to exist and stay in business?” They always say, “Yeah.” They don’t articulate it, which is fine. I’m trying to set them up, I say, “Yeah.”

Banks have to do two things. They have to get deposits. They need people, personal deposits and business deposits, to open up checking accounts and savings accounts. When they do that, a bank has what we call AUM or Assets Under Management or deposits. I should say more so because they’re deposit relationships. There’s a formula across this country where if you have much money in deposits, a percentage of that, the bank can now leverage and lend.

The second thing they have to do to be in business is to lend money for a profit to be a business. The bank has to do two things, they have to get deposits and then they have to take your deposits and they have to lend it at a higher rate so they make money. Here’s the thing, you think you’re safe. You think it’s better to keep it here in the bank. What you didn’t realize is that you’re already lending money to real estate deals. You’re not getting paid for it. How would you like to cut out the middleman?

Sign me up.

It’s fun. When we started, I didn’t have this thought track in 2004 when I’m in the bedroom of the four-story walk-up brownstone. I didn’t understand that. I was just trying to raise money for a deal. With all of the systems that I described and with all the knowledge that we educate on, our real estate investors have no problem raising money. It takes work. It’s hard. The first time you go to pitch for raising money, I guarantee that you’ll sound crappy but that’s why we practice through education and training that we do. Those are some of the highlights.

I don’t have a lot of interest. I remember being in college, I had this one roommate, John K. He’s a nice guy. He played rugby. I wrestled. I don’t think we talked, maybe twenty sentences throughout the school year. We got along great. We didn’t talk much. We did our thing. We shared a room in college. I remember the last night when we’re moving out of the apartment for the year. We stayed up all night talking to get to know each other. He said, “Paul, what are your hobbies?” Even back then, I was at a loss. I said, “I like rolling change.” To this day, I don’t have a lot of hobbies but I love real estate. It’s not that I’m over fascinated with money but the game of money is a lot of fun. Me and my partners, that includes you, Jeff, when you learn something that helps not only yourself but can help other people, you’re passionate and excited to share it. That gets me rambling.

I want to say one more thing on this question you asked and some tips for people reading. How do you raise money for your deals? How do you get money for your deals? One thing that people don’t realize is the way that we started and can help and teach other people to start is you have to start by doing creative real estate. What does that mean? It’s a broad statement. I told you we bought that first 876 Elm conventional financing. I went to a bank and put whatever it was, 20% or 25% down. You’re then out of money. That doesn’t work if you’re trying to get on the treadmill of buying and owning a bunch of real estates.

What we started to learn is that you can buy properties with no money. You can take a property subject-to. If you’re learning about that for the first time, that’s not assuming the loan but that’s taking ownership of a property. The deed goes from the sellers’ name to your name with the mortgage still in place and you honor that mortgage by paying it and keeping the insurance requirements the same way and keep it in place. You don’t use your credit. You don’t ask the bank for a loan. It comes with the house. You can do seller financing, someone who owns a house either free and clear or not free and clear can be the bank like we taught the private lender and they can take back a note.

Get Your Capital: If you’re banking at a large national bank, stop. Go to the local regional community bank and start your banking relationship there.

When properties are in trouble, you can short-sale the property from banks and work on that. There are a lot of creative strategies. Frankly, when we started in 2004 for those first five years, we did a lot of creative financing. We did a ton of subject-to. We did a ton of seller financing. Do you want to know why? It’s because we had no money. We had to be creative. Unfortunately, when you have resources and means, we’re not as creative anymore. It’s like, “We’ll buy it for cash because we have to.” I love that period where you’re forced to innovate and be creative.

The thing I can excite people with is we have the answers to the test. We’re not the first ones to do it. There is a roadmap. There are tools on how to buy a property with no money. If you have more money, it’s easier to buy more properties and you’ll get there. There are tools when your credit sucks where you don’t need your credit. Those points, as we learned them, got us more in love with real estate and the business. I know everybody’s not like this but we love to learn. People ask, “Why do you have an education?” I love this question. It’s always a question. If you’re successful, why do you teach it? It’s a valid question. I’m on board with it.

You have to understand the origin of how we got started. My two partners went to Yale. I went to the University of California. None of that education taught us what we do now. We had to learn from whoever would teach us and we’re grateful for that. That’s not why we teach. As we’re learning, we started to grow our business in CT Homes in New Haven, Connecticut. Frankly, this is how we met you. In our local real estate club, we would host what we call rehab subgroups. Once we were learning, we said, “We’ll volunteer to teach the mistakes we’re making and the lessons we’re learning.” We did that so that we could meet more people who would be private lenders to our deals and that would buy our deals if we wholesale them to them or buy rehab deals. We did it as a necessity to grow our business.

What we found as we started sharing our business processes and systems, we loved it. This is the Fortune Builders principle. A lot of people also ask, “What’s behind the name Fortune Builders?” A true fortune builder is someone who learned something and then re-teaches it. When you teach something, you learn it twice and you master it. What we found as we were tasked with recommunicating and re-teaching, our systems got better. We got improved execution because if we’re saying we’re going to do it, you got to keep the discipline and we improved upon it. We started it as a necessity to grow our business. It’s something that we love.

One thing on the private money, you used to tell me something in the beginning. I thought you were crazy when you said it. You said, “Jeff, it’s going to take work to get out there and start raising private money. Maybe it’s awkward. You’re going to stumble at first. There will come a time where people are begging you to loan you the money instead of you asking.” I remember approaching the first couple and going with my tail between my legs, “Would you want to give me $500,000?” I closed a deal in Virginia and there were two text messages, “I need $100,000. Who wants it?”

It’s you awarding the opportunity to someone. I teach this topic, which we’re not teaching it necessarily right now. In the class I came out of for two days, The Money Academy here at Fortune Builders, I tell people there’s a paradigm shift. Before you go asking for money, you’re not asking for their money as much as you’re giving them an opportunity. You’re either putting your money in a checking account, a savings account, a CD or the ups and downs, the stock market. Who has the opportunity to lend their money secured by a real asset that you buy at a discounted value? We have a buying formula. We have a buying software, our mail formula, our deal analyzer and it’s insured. It’s securitized on the land record. Nothing can happen until that asset is transacted and you have a promissory note with all the terms to pay you back. Who has an opportunity? It’s not out there.

In our little circle, everyone thinks that’s common knowledge. It’s not. If you move your feet and you move your mouth and you’re month over month, year over year, consistently and you’re the real estate person in your friends, family, church, community. Eventually, as you’ve experienced, Jeff, people are calling you, “Jeff, I have a friend. They have a house. They need help. Can you buy it?” or, “I have a friend. He’d love to learn more about how you’re paying him 10%? Will you take his money?” They need us. Money needs those willing to put in the work, put in the education and do this more than we need them. I know it doesn’t seem like that but there’s more money out there than there are of us doing this.

We get into that at that one-day virtual event. Paul and his business partner, Than, get into some of those techniques. I encourage you to check that out at FortuneBuildersShow.com. We have the answers. I love this story leading up to it to what you’re doing now. Everybody knows somebody who is buying and selling real estate in their local market. Everybody wants to be in it that’s why the shows are popular. You are on Flip This House for quite some time. What do you think stops most people from either being successful in real estate or even giving it a shot at all?

When you teach something, you learn it twice. You master it.

The easy answer is fear. You have to redefine fear but fear is not a stop sign. Pay attention to what you don’t know to have the confidence to overcome that fear. In my opinion, real estate is as American as apple pie. With 100% conviction, I can say this. I don’t care who you are. This is well outside the United States. At some point in your life, you ask yourself, “How do I benefit more from real estate? How do I make money from real estate? I own a home or whatnot but how do I get in the real estate game?” At some point, that floats through their head.

For some people, it’s not the journey they want to go on and need to go on. It’s perfect. I have some great friends that are amazing professionals in their profession and they supplement with real estate. They do passive lending to us at CT Homes or an equity partner at our commercial platform, Equity Street Capital. It wasn’t their calling. For a lot of us, in our circle, it is something they want to do. The question is what holds them back? It’s fear. Why I like to share the story is that you have to be strong enough in your life. I’m not just talking about real estate but it is answering the question. If you don’t like what society is selling, don’t buy it.

We’ve all had different talk tracks. We’ve all been brought up not good or bad but our parents saying one thing, commercials on TV saying one thing, magazines saying one thing, “Go to school. Get a good job. Do this. Do that.” We’ve all been messaged these different things that boxes in. I know that it’s hard to have a conviction, “I need to do this. I want to do this.” Some of my closest friends and family are saying, “Why are you doing this?” That’s where you need to surround yourself with people that have done it, that are encouraging, want to do it and along the ride with you.

That’s what’s amazing about our community of investors. You’re a part of it in the success and a coach. We have this group of people that are not cutting each other down. They’re helping each other. We have people that are six months in helping someone that got started. We have people like, in your case, fifteen years in or so helping and vice versa. Fear and then having the strength to say, “I can’t listen to everyone. I got to listen to myself. This is what I want to do. It’s going to take a risk.” That’s the other thing I would stress upon.

We, you, me, our community, we do real estate but we’re a bunch of self-development junkies. When I say risk, we’ve all had to learn that risk isn’t a bad thing. Risk is part of the process. If you want more than you’ve got, you got to educate. Don’t take a wild risk. Take a calculated risk. Fear and risk, redefining those differently, are a big part of it. Fear is to pay attention to what you need to learn more to have the confidence to overcome it. Everything takes risks. That’s the point. When you’re educated in systems and learning from people that have done it 100 yards ahead of you and can give you that roadmap then you’re eliminating a large portion of the risk.

You can’t eliminate risk but you can decrease it through education. The higher the education, the lower the risk. The lower the education, the higher the risk is what it comes down to. From the beginning, you’re somebody flying across the country to go to training and things like that. I know you closely now. You don’t stop learning. You don’t stop growing. You always point to education being the greatest. It was Benjamin Franklin that said, “The greatest investment a person could ever make is in their education.” Once you know something, the formula to raise private money, no one can ever take that from you. You can duplicate it over and over again. What would you say is the greatest investment you’ve made outside of education?

You took my first answer. Education always pays you tenfold. Let me try to answer it in terms of a real estate deal. The best investment I ever did was buying my first real estate deal. Not because it was perfect, not because it was a good deal and not because I didn’t have heartache, headache, lost money, a lot of sleepless nights. I had all of those tree roots into the sewer line going to the street and backed up the sewage in the basement. I’m down there in boots cleaning it out myself.

You’re asking, “Paul, how can you tell me 876 Elm was the best deal you ever made?” To do that deal, I had to put my money where my mouth is. I had to overcome risk. I had to overcome fear. I had to do something I knew I wanted to do but everybody else was giving me an easy out, “Don’t do it. You’re crazy. It’s the wrong time. You’re stupid. Much smarter people have made money in real estate than you and lost money.” That first deal, I had to overcome all that. What you learn in business, which is contradictory to our traditional education system is that you get rewarded for starting and getting rewarded for making mistakes.

When you make a mistake in business, you learn what not to do. You learn what you need to gather more information on, have a better system, have a better approach. I value my traditional education. Through my self-development, I try to teach my kids. I got two boys and a little girl. I said, “What did you fail at? Let’s celebrate it.” If you didn’t fail at something, you played it safe. You weren’t doing something that was stretching you. We try to celebrate failures. If you want to work your next 40 years for Pepsi, start driving around salesman and get to $85,000 or $100,000 when you’re 60, retire and go that route, there is nothing wrong with that. For me, it would have been a slow death if I did that track and I didn’t honor my inner voice what I knew I wanted to do.

Get Your Capital: When the Government needs more money, they print it.

To bring it full circle, that particular deal, 876 Elm, was good. It was bad. I can tell you every story there. I could tell you the names of the tenants. Evelyn Beauduy was on the first floor when we bought it. She was there for a long time when we owned it. I moved to San Diego and we still owned it. We had property managers. I managed it. If you don’t hear anything else from me on this share, get started in real estate. If you want to do real estate, do it. Do it by enrolling people. Ask for help. Successful people and people that make money ask for help. There’s a myth, like, “I need to know everything.” You probably won’t know anything. If you’re smart enough to ask someone else who’s done it before, you ask them, “Can I follow your roadmap?”

We bought that house and closed. We did a 1031 exchange. My partner, Than and I, we own that house from 2004 until 2019. We go to sell it, that and another three-family across the street. That was 876 Elm. A year later, we bought 875 Elm. You know Elm Street. You know the houses. We sold both those houses in 2019 for about $640,000. I could be off $10,000 or so. We bought them each for $180,000. The other one, we bought for $160,000. We sold each of them for about $300,000. We sold them both to the same buyer. We had a total sales price of $600,000.

The IRS wants you to save for your retirement. The IRS also wants you to keep your money in the economy for jobs, production. The government can always change things but the IRS has a sponsored 1031 exchange rule that says that if you have a property, you can exchange that property for a lifetime property. If you have a property that’s producing income and exchange it for another property that’s producing income, you don’t have to pay taxes on your gain. We bought them for $180,000 and $160,000 and change. We sold both of them for over $600,000. We’re talking $300,000-plus of taxable income, capital gains income.

We sit here in California and have a high income. That’s a 30%, 40%, almost 50% tax on that money. The IRS says, “If you exchange those properties for another piece of real estate and keep your money in the economy, you don’t have to pay taxes on your gains. You can defer it till a later date.” We exercised a 1031 exchange. We sold those in 2019. In 2020, in the middle of the pandemic, we bought a $23 million commercial retail asset where we exchange those dollars into two other partners and one of them is a financial partner. What we do is we have a commercial syndication symposium that we teach here.

People always ask, “I get it, private money, hard money and everything for single-family. That’s how you finance that. How do I get $5 million of equity? How do I get $500,000 of equity for the 25-unit apartment building I’m going to buy?” In our case, the 460-unit apartment building that we’re going to buy. It’s a process called syndication. Whether you do it with 1 or 100 different individuals, we syndicated that property with one investor, us and our partner. We exchange that 876 Elm and 875 Elm.

Here’s the punchline. On a perfect year, when we owned those two rentals on Elm Street in New Haven, Connecticut, if the tenants all paid on time and there were no issues with the house, my spreadsheet told me I’d make $20,000 of cashflow a year. Never in a year did every tenant pay perfectly and there weren’t repairs for rental and that’s okay. That’s the business of owning real estate. That was our potential cashflow.

The exchange we did through everything I’ve taught and told you that we teach, by buying this commercial property and syndicating it, our $20,000 from that money increased to $120,000 projected by executing that. That’s the story of the first deal and all the lessons I learned. More importantly, you have to overcome what we’re talking about, fear, the idea that everything is safe and there is no risk. In real estate, you get information and education to mitigate and reduce the risk down to a little bit of risk. Every deal has risks that you don’t know. There’s an outcome that is unknown.

I’m going to resell you on why you’re reading this show and real estate. From 2004 to 2019 when we owned 876 Elm and 875 Elm, the tenants were paying down my mortgage. I borrowed money from the bank. Even if the property didn’t appreciate it, they were creating equity for me. They did. I was depreciating and getting tax benefits every year owning that property. The statement is never buy something where it has to appreciate. If you own real estate long enough, the government is going to do its job. They’re going to supply money to the economy. They’re going to print money. They’re going to continue with inflation. That means the value of hard assets goes up.

The interest rate was 6% or 7% at the time. We’re borrowing money at 7%. We’re making more than that return. Our tenants are paying down the principal. We’re creating equity there. On top of that, when we went to sell, it happened to be that we sold it for almost double of what we bought it for. The IRS says, “We want to help you not pay taxes.” Government-sponsored rule, IRS rule 1031. We put it into a commercial property. All those things are fun. I’m super excited for everyone reading because no matter where you’re at in the journey, I always say this, it’s a marathon and not a sprint. The longer you stay in real estate, the better off you’re going to be, the easier it gets, and frankly, the more fun.

It’s not the money you make or the assets you gain; it’s the person you become.

You’ve experienced this, Jeff, “I’m going to slow down. I’m not going to try to do as many deals and all this stuff.” Frankly, you don’t need to. I got my asset base. I got my cashflow. I’ll slow down. You end up doing better deals. Sometimes you end up doing more deals because of the consistency, how you’ve marketed yourself and the people you’ve benefited. You’d pay off private lenders and rehab lenders. Deals keep coming to you. That’s what’s fun. People say, “Paul, what are you going to do when you retire?” I am retired. I’m going to do real estate.

Don’t get me wrong. When you start, it’s hard and nerve-racking. That’s why I can tell the story of sitting in that bedroom in the four-story Brownstone. I couldn’t sleep that night and nights after that. I wouldn’t trade anything from then to here. It’s not the money you make. It’s not the assets you acquire. It’s the person you become in that journey. That journey developed my character. It taught me about integrity. It taught me about saying what you’re going to do and do what you’re going to say. If I had done the easy route and got that job at Pepsi, which I didn’t get, I would not be here, have all these lessons and be able to help, support, teach and be as good a father, husband and son as I am now. Life is for living.

My older daughter put this big sign above her desk that she painted and it says, “Five seconds of fear or a lifetime of regret? I choose five seconds.” That’s what it’s about, pressing through that fear of getting started. Paul, I’m going to get you out of here on two more questions. What are the top three tips you would give somebody reading that is not in real estate, they want to get in and they want to get started?

Number one, keep doing what you’re doing right now. Anything that you can be around, listen, educate whether it costs money and time or doesn’t, keep doing that. That’s your educational process. The timing for all of us is going to be different. Number one is to keep learning. As you learn on all topics of real estate, you’re going to start to navigate where you want to start. Number two is you have to surround yourself with the right people. That’s at both levels. If you think you want to get into real estate, you have to pick and choose your tribe.

Who do you want to learn from? I will always advocate people do a lot of research. Are the people that are teaching you doing the business? Are they buying and selling rehab properties? Did they used to do it in a different market and they’re teaching you something that used to work? This market is always different from what yesterday’s market was. From residential and commercial, you got to make sure you’re learning from the best. The community that you pick to learn with will either accelerate and help you stay on task and positively reinforced or you won’t get that support and momentum.

Number three is you’ve got to change your habits. Sometimes it’s not about changing as many habits as it is dropping some habits. Let me paint a picture. If you find yourself getting up, you’re taking care of your family, making them breakfast, you get them to school, you go to work, now you’re taking care of your boss and your job. You come home. You’re doing the dinner. You’re taking care of your family. By the time you get to relax, you’re like, “I’m going to relax here.” You go sit on the couch or the Barcalounger, you turn on the TV and then you wake up because you fell asleep. The whole thing happens again. All of a sudden, 5, 10 years of your life goes by.

It’s always about discipline and it’s about creating new habits. It’s not always new habits stopping some old habits. Don’t watch TV. It’s crap. If you don’t watch TV, you’ll find 2, 3, 4 hours a day that come back in your life a week. Your eating habits. If you’re not physically exercising, you’re not feeling good. Start to look at things you need to stop doing to become the person you want to be. All of those things matter. When you say, “I’m interested. I want to start the journey of being a real estate investor.” What you’re saying is, “I want to be someone different than I am now, not in a good or bad. I have a goal.”

I can tell you honestly that I always saw myself as a successful real estate investor. Did I believe it? I don’t know. When I’m sitting at the bar, I always knew there was something better. I always knew there was a journey to go. I didn’t know that I would go from bartender to owning $1 billion in real estate. Your conviction and faith in yourself are important. To do that, you got to learn from people who’ve already done it because that’s the answer to the test. You can shrink time and reduce mistakes if you get the roadmap. Number two, you got to surround yourself with people that are positive and supportive. Number three, you got to look at, “What is now my daily routines and habits that I need to amend, adjust or eliminate to get closer to where I want to go?”

These may be similar answers. A lot of people follow this show. They’re doing the business. They do 10 to 20 deals a year, whatever it is. They hit the ceiling. You scaled your business. One thing that’s amazing about CT Homes, your residential redevelopment company, $40 million a year like clockwork and you’re never there. It’s systematized. You have all the right people in place. Any words of wisdom for that person that hit the ceiling, “I want to scale. I want to grow. How do I do it?”

Even more so, if your life and growth plateaus. You work out, you hit a plateau and you’re like, “How do I change things up to get stronger, faster, quicker?” Business is the same. Even more so those people that are doing the business. I don’t care what level you’re at. I’ve got to experience most of the levels. There’s some I’m still going into. You need to do those three things I talked about. You need to selectively identify and say, “I need to be around that person. I need to learn that.”

Before the pandemic, I did an online class at MIT on real estate finance. Why? It’s because I wanted to sharpen the saw. Keep learning. Keep looking at who you can learn from or be around or bring into your network that’s going to give you a new and different perspective. You will hit plateaus. I have multiple times in my business journey where I couldn’t get to any next level. To break through plateaus, you will have more failures. You’ll make mistakes. At the moment, you will think to yourself, “I can’t believe I did that. I was doing pretty well. I was successful. I’m stupid. Why did I do that?” A monumental failure and you’re now regretting that you did it, don’t do that. That failure was designed for you. Learn from it, analyze it, postgame it and then attack it differently. Achieve that goal. That’s when you’re going to get to another level.

There’s so much wisdom. Paul Esajian, thank you for joining this show.

It’s super fun.

It’s such an honor to have you here. I hope everyone reading has enjoyed this time. If you want to learn from Paul or learn from Fortune Builders, go to FortuneBuilders.com. You won’t regret it. There’s a lot of great information there. We’re on a mission to get this financial education to as many people as possible. Share this. If you got any value from this on Instagram, Facebook, YouTube, tag a friend on it and get the word out there. We’re looking to reach as many people as possible.

If you want to interact with us, you can follow us on Instagram @FortuneBuilders. I encourage you to ask us questions, send questions. I’ll be doing live Q&A sessions following most of the shows to get as much information to you as possible. If you want to connect more with Paul and learn more about him, you can go to FortuneBuilders.com/podcast. We will see you next episode on the Fortune Builders Real Estate Investing Show. Thank you so much.

Important Links:

- Fortune Builders

- CT Homes

- Are You Dumb Enough to Be Rich

- FortuneBuildersShow.com

- Facebook – Fortune Builders

- YouTube – Fortune Builders

- @FortuneBuilders – Instagram

- FortuneBuilders.com/podcast

About Paul Esajian

Paul Esajian has over 14 years of professional experience in the real estate investment and lending industry.

Paul Esajian has over 14 years of professional experience in the real estate investment and lending industry.

He is the founder and principal in several real estate investment companies and has been involved in over $750 million of real estate investments during that time frame.

Paul has experience in many facets of real estate investment including underwriting, raising capital, investor relations, construction management, accounting, taxation & business management.