Key Takeaways

- By researching tax tips, real estate investors can maximize their returns this time of year.

- One of the best real estate tax tips is to learn which deductions apply to you, and how to use them.

- Read our infographic below on the best tax strategies for real estate investors.

Many investors take a reactive approach to tax season, year after year. The danger in waiting until the last minute, however, is that you can miss out on valuable deductions by failing to plan ahead. Investors hoping to save themselves time and money should seek to adopt a more proactive stance: one that involves the right planning and implementation of key tax tips.

While consulting a professional is one of the most effective ways to prepare for tax season, a little research can go a long way. Investors who familiarize themselves with tax policies, real estate deductions and common mistakes will both maximize their returns and reduce overall stress. Continue reading for real estate tax advice that can help your business succeed each time tax season rolls around.

Tax Planning Tips For Real Estate Business Owners

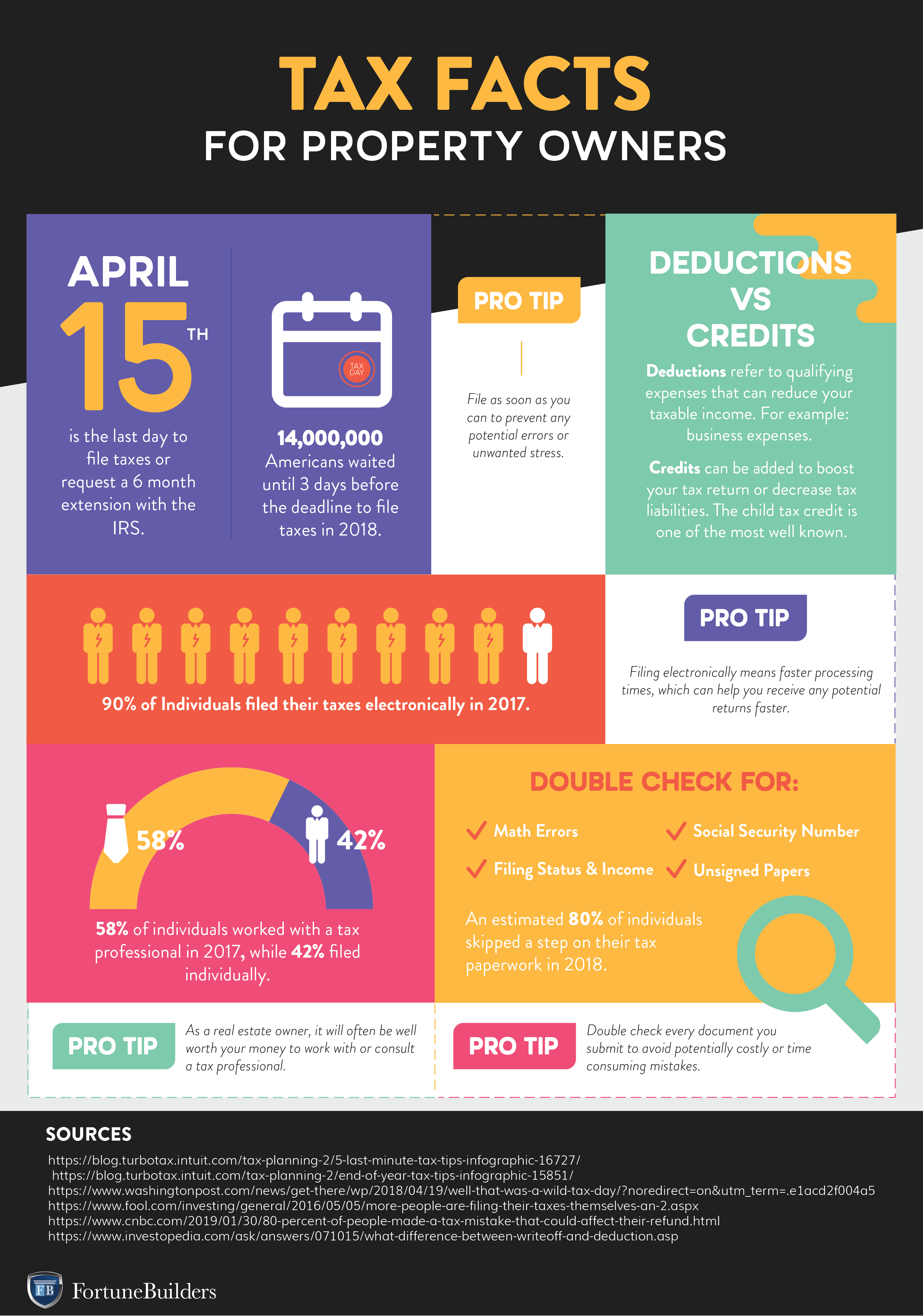

One of the first things real estate investors can do to prepare for tax season is to familiarize themselves with the tax filing process. This includes learning common terminology as well as how to file. The infographic below shares common tax advice that can help:

Real Estate Tax Tips To Save You Money

To ensure you take the biggest advantage of tax season, it is important to look at a variety of topics and resources. Here are some tax tips to guide you through tax season and increase your returns in the process.

Use a CPA

A certified public accountant (CPA) is a trained financial advisor who can greatly help your real estate investing business during tax season. CPAs will often provide a variety of services including investment planning, acquisitions and more. Investors should seek out a CPA that specializes in real estate specifically, as they will have a better understanding of which forms and deductions apply. There will be fees to work with a CPA, though these costs are often nominal compared to the amount of money investors can save in the long run by filing their taxes correctly.

Reinvest In Another Passive Income Property

Given the benefits associated with real estate investing, it only makes sense to build your portfolio over time. A great way to do that is by reinvesting profits into a passive income property, which can help generate long term cash flow. Passive income properties benefit from depreciation deductions, stable income and more.

The reason this strategy relates back to taxes is because after the sale of a property, many investors will be subject to the capital gains tax. This is a tax on the profits made from the sale of an asset. If you had a particularly successful year investing, it may be beneficial to look into investing in another property. To learn more about how to reinvest real estate returns, be sure to read this article.

Consider IRAs

While direct real estate investing carries many tax benefits by itself, do not sell yourself short by forgoing the advantages offered by regular contributions to a self-directed IRA. A self directed IRA is an individual retirement account that allows an individual to make all of their own investment decisions. Investors have the opportunity to invest in stocks, bonds and even real estate. IRAs investments are often allowed tax free or tax deferred growth, though the funds are inaccessible until investors reach a certain age.

Get Organized

Organization is a key trait of any successful entrepreneur, and it is especially important when tax season comes around. If you work from home, or even have your own office, focus on setting up a space that allows you and your team to thrive. An organized office will allow you to increase productivity and organization, both of which can make for an efficient filing process. If you are interested in learning more about how to work from home effectively, check out this guide.

Differentiate Between Short And Long-Term Investments

As you prepare for tax season, start by separating your short and long term investments. Short term investments are those you’ve held for one year or less, while long term is anything over that time period. For example, wholesaling, prehabbing, and flipping typically fall under short term investments while buy and hold properties are typically long term. The difference will be important in determining the tax rates on each investment. Ask your CPA to help you figure out which entity structures are right for you and your investments.

Be Wary Of Travel & Entertainment

As you track your operating expenses and deductions, be careful not to forget about travel and entertainment costs. Property managers and landlords will be able to deduct any travel associated with property viewings, lease signings or maintenance from their overall taxable income. Many investors fail to realize how travel costs can be beneficial during tax season.

Entertainment costs can refer to anything from attending real estate conferences to hotel and airfare fees to hosting business-related client events. To take full advantage of these write offs, always keep clean records and double check which business expenses are eligible.

Track Your Expenses

There are a number of tax deductions real estate investors will be eligible for; however, they must keep well maintained records in order to make the most of each deduction. Track each and every business expense, and keep proper records throughout the year. Some examples are the cost of appraisal fees, business cards, commissions, advertising, escrow fees, insurance, vehicle expense and more.

It might seem trivial, but keeping your paperwork and accounts organized year round will make a huge difference come tax season. In addition to ensuring you don’t miss any valuable deductions, tracking your expenses properly can save you money in accounting fees. Many CPAs will charge less for investors with well-organized records.

Go Digital

When people think tax season, they often picture business owners scrambling through disorganized paper receipts and files. Avoid this trap by using digital programs to organize your paperwork. Tools like MileIQ, Evernote, and Mint and great for bookkeeping, as they allow users to categorize expenses and even take notes on specific inputs. Using a digital organization system year round can save you time, money and endless stress when tax season rolls around.

Think Green

Some often overlooked tax deductions come from installing environmentally friendly features throughout your rental properties and rehabs. While these deductions may not be as abundant as they were in years past, there are still a few tax breaks for energy-efficient improvements. For example, there are deductions available for the cost of solar panel installations and solar water heaters. Property owners should consider how these tax deductions can help them over time.

[ Thinking about investing in real estate? Register to attend a FREE online real estate class and learn how to get started investing in real estate. ]

How To Fix Common Tax Return Mistakes

The tax filing process requires a strong attention to detail, but even the most meticulous investors will make a mistake from time to time. The two most common tax mistakes are: over reporting income or accidentally combining personal and business expenses. Luckily, many of these mistakes are not the end of the world; they simply require some extra paperwork.

Form 1040X was created to handle reporting errors and correct any issues made upon initial filing. In the event you notice an error on your tax paperwork, fill out this form and submit it to the IRS as a correction. You may also need to attach any forms or schedules that will be affected by the change. Remember, common tax mistakes will happen from time to time, just be sure to correct any discrepancies as soon as you realize them.

Summary

Don’t wait until the last minute to file your taxes this season. If you wind up scrambling over paperwork, you can’t be surprised when your returns are lower than expected. The best way to avoid this situation is to adopt a proactive approach and review our pro tax tips to help maximize your returns. Once you understand taxes for real estate investors, you can help your business realize success year after year.

What are your favorite tax strategies for the savvy real estate investor? Share your tips in the comments below.

Ready to start taking advantage of the current opportunities in the real estate market?

Click the banner below to take a 90-minute online training class and get started learning how to invest in today’s real estate market!